Housing supply swells in cool spring market

Calgary’s housing inventory was on the rise once again in May as new listings climbed and sales slowed to 1,923 units.

“While recent oil price gains may have some feeling optimistic, weakness in the labour market continues to impact housing demand,” said CREB® chief economist Ann-Marie Lurie. “Job losses are spreading into other sectors, wages are declining and unemployment levels remain high. At the same time, we’re seeing housing supply levels rise in the rental, new home and resale markets.”

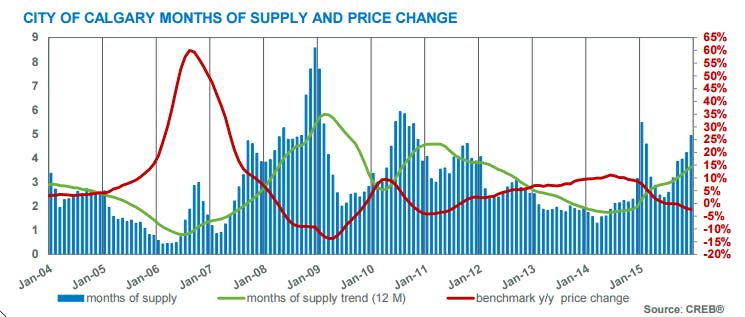

Inventory levels rose by 14 per cent in May to a total of 6,148 units. Every product type is experiencing these gains, but the largest inventory growth has occurred in the apartment and attached categories.

Together, these sectors represent half of all resale inventories in Calgary. “The resale apartment market has been the most difficult for sellers,” said CREB® president Cliff Stevenson. “They are competing with improved selection in the lower price ranges of the detached and attached markets, and facing increased competition from the new home sector, where builders are offering incentives to attract potential buyers.”

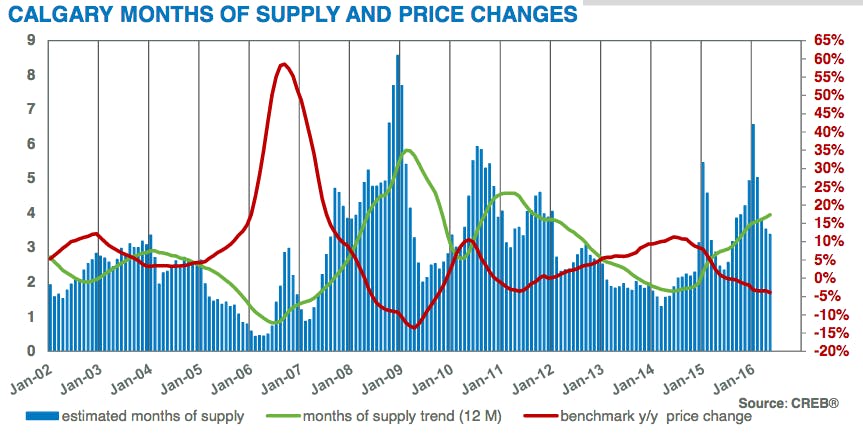

While apartment resale supply remains 22 per cent below the May high of 2,055 units in 2008, the combination of rising supply in the apartment sector and steep declines in sales activity has elevated months of supply to nearly six months.

The apartment sector of the market has experienced buyers’ conditions for more than 10 months, so the impact on pricing is more dramatic, compared to the detached and attached sectors.

In May, the apartment benchmark price totaled $278,500, a monthly and year-over-year decline of 0.7 and 5.6 per cent. In the detached and attached markets, home prices totaled $500,500 and $332,100, a year-over-year decline of 3.4 and 4.3 per cent.

Click on the following link for the May_2016 Calgary Housing Market Statistics Report

Elevated supply levels placed downward pressure on prices in December:

Elevated supply levels placed downward pressure on prices in December: