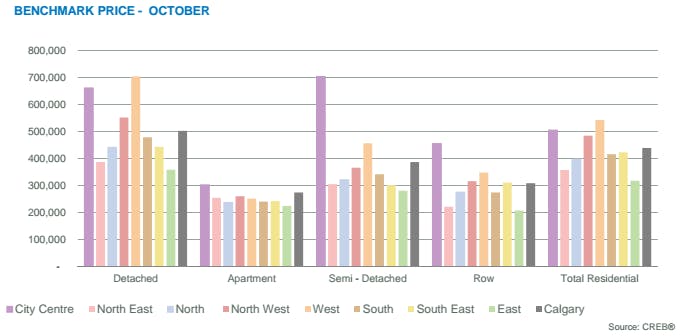

Detached prices stabilize in soft market

For the first time in two years, sales activity in October resembled normal levels. City-wide sales totaled 1,644 units, which is an increase of nearly 16 per cent over last year.

“The shift in sales activity this month is likely related to the new mortgage rule changes, inventory gains in the lower price ranges and further price adjustments,” said CREB® chief economist Ann-Marie Lurie. “The combination of all these factors may have encouraged some purchases to take advantage of the market conditions, particularly in the lower price ranges. However, with several factors at play, the monthly shift in demand may be temporary and will need to be monitored over the next several months.”

Sales activity rose across all product types in comparison to last year, but the largest gain in sales occurred in the detached sector at 18 per cent.

There was a noticeable shift in sales activity by price range in October. In the detached market, homes priced between $300,000 and $400,000 saw the largest improvement in sales, while attached and apartment sales growth was mainly occurring in the lower price ranges.

“This year has been a challenge for many sellers,” said CREB® president Cliff Stevenson. “So when we have a rise in sales, it means more buyers got into the market and more sellers got out, which is a positive for consumers on both sides of the transaction.”

“Sales activity changed direction in October, but we need to see some consistency next month and the month after to call it a trend,” adds Stevenson. “For now it’s a nice building block.”

Despite the monthly rise, year-to-date sales activity in all sectors remained lower than last year’s levels and well below longer term trends. In fact, year-to-date sales activity has totaled 15,642 units, which is 6.3 per cent below last year’s levels. While increased activity in the lower price ranges had a greater impact on the average and median price, benchmark prices once again edged down in October.

The city-wide unadjusted benchmark price totaled $438,900, or 0.34 per cent below last month and four per cent below last year’s levels.

Since the start of the downturn, home prices have declined from a low of 3.8 per cent in the detached market to a high of 9.4 per cent in the apartment condominium sector. And, despite the rise in October sales, monthly prices continued to decline for most product types in the market.

Click on the following link to view the full .pdf report! October-2016-statistics-package-for-the-city-of-calgary

Click on this following link to view the full .pdf report for the Regional Statistics: october-2016-regional-statistics-package-for-calgary-and-area

housing market

Monthly Statistics Package as of May 1, 2016

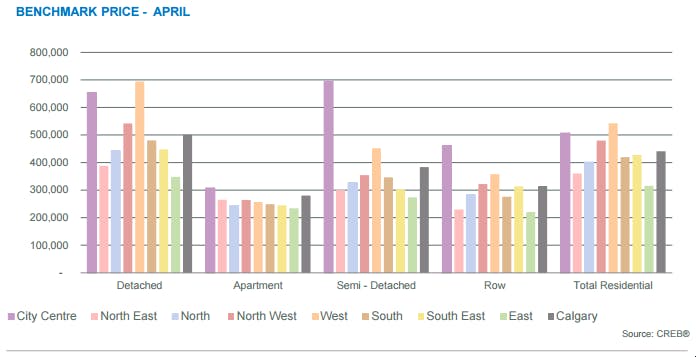

Minding the gap – Sellers continue to adjust pricing expectations

Market imbalance in Calgary’s residential resale housing market continued to weigh on citywide prices in April. Much like the previous month, year-overyear sales fell while new listings increased, resulting in inventory gains across all sectors of the market. As a result, benchmark prices in the city declined by 0.4 per cent from last month, and 3.4 per cent from last year, to $441,000.

For sellers, the reality of seven consecutive months of price declines has started to sink in, said CREB® president Cliff Stevenson. “From re-considering the listing of their home to lowering expectations on price, sellers are beginning to adjust to the current market reality,” he said. “However, some buyers in the market are still not willing to pull the trigger because they expect even bigger discounts. And so that gap between buyers’ and sellers’ expectations still persists across many product types and locations.”

Despite this, the detached sector fared better relative to the other sectors of the market. While detached sales activity has fallen by over four per cent so far in 2016 compared to last year, the sales to new listings ratio improved in April. This prevented sharper inventory gains and caused months of supply to move toward more balanced levels. The same cannot be said of other market sectors. Year-to-date apartment and attached sales declined by a respective 19 and 13 per cent compared to last year. Slower sales, combined with rising inventories, ensured that market conditions continue to favour buyers in these segments.

“While the weak economic climate is influencing demand, the apartment and attached sectors are further impacted by increased supply in the competing new home sector and rental markets,” said CREB® chief economist Ann-Marie Lurie. “This is one of the contributing factors to the steeper price declines recorded in the apartment sector.” Since the start of the price declines monthly unadjusted benchmark apartment prices have declined by 7.6 per cent, while semi, row and detached have declined by a respective 5.9, 4.6 and 4.1 per cent.

Click on the following link: April_2016 for the full report!

YYC March 2016 Team Penley McNaughton Newsletter

Click on the following link to view the full Team Penley McNaughton’s YYC Newsletter and view the most current February 2016 statistics!

Housing market conditions favour buyers

Weak sales activity relative to inventory places downward pressure on prices

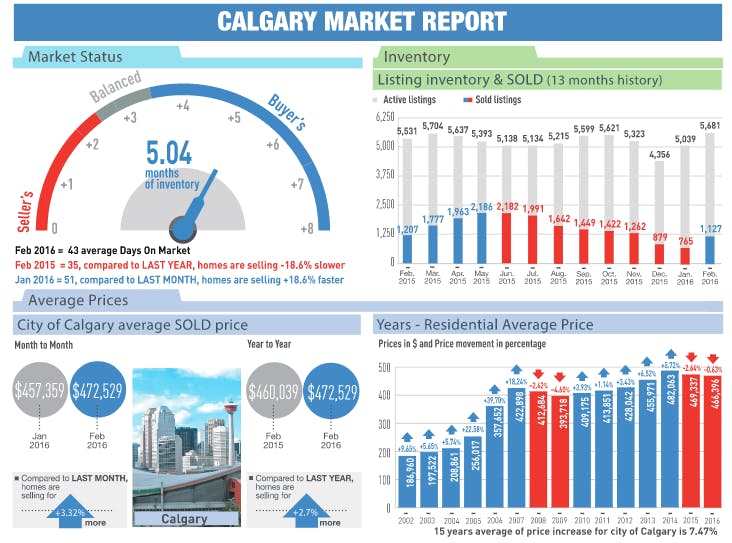

Persistently high inventory levels within Calgary’s residential resale housing market, combined with weak sales activity, contributed to buyers’ conditions in November.

Monthly sales totaled 1,263 units, a 28 per cent decline from last year and nearly 20 per cent below the 10-year average. Meanwhile, the amount of new listings in the market increased by five per cent over last November, and moved five per cent above 10-year average.

The combination of both soft sales and elevated listings caused months of supply to rise above four months. It represents the third consecutive month that housing supply in the city has remained near four months, which is an indicator that supports buyers’ conditions.

“The housing market is reflecting the realities of the economic conditions,” said CREB® chief economist Ann-Marie Lurie. “Calgary has continued to post job losses in the energy sector, unemployment levels are high, wages are down and recovery expectations have changed. All of these factors have contributed to the weak demand we have seen throughout the year.”

CREB® president Corinne Lyall pointed out that inventory levels still remained 27 per cent below the November highs recorded in 2008.

“Furthermore, price declines have not been as steep as those recorded during the last downturn,” she said.

The unadjusted benchmark price in November declined to $450,700, a 0.5 per cent drop compared to last month and two per cent from last year.

Calgary’s detached housing sector faired the best in November as months of supply increased to only 3.4. Nonetheless, the unadjusted benchmark price declined by 0.6 per cent compared to October, and 1.52 per cent from November 2014, to $510,700.

In the attached category, buyers’ conditions emerged as months of supply increased to 4.8. As a result, the unadjusted benchmark price declined to $352,400, a 0.5 per cent drop from last month and 1.5 per cent from last year.

The apartment sector continued to be the hardest hit of the three sectors. Months of supply increased to 6.9 in November, causing benchmark prices to slide 0.5 per cent from October to $287,000. Meanwhile, year-over-year prices were off by 4.6 per cent.

Despite weaker absorption rates for most of 2015, residential benchmark prices have only recently started to decline – while average and median prices have dropped more dramatically. Lurie attributed that to slower activity in the higher-priced segments of the market, which can skew average and median prices.

Benchmark prices represent changes for similar-type homes, minimizing the impact caused by changes in distribution.

“It is not a surprise that the average price has recorded a steeper decline than the benchmark price,” she said. “Last November, detached sales in the city over $700,000 totaled 159 units or 15 per cent of the market sales. This November, there were only 103 sales representing 13 per cent of the market sales.”

Lyall said knowing the difference between indicators such as average, median and benchmark prices is important for sellers.

“There is no question that this can be a challenging market,” she said. “However, because of these circumstances there is a greater need for market intelligence.”

Click Here, on the following link or on the image below for the full .pdf of the November_2015_Monthly_Housing_Statistics

2015 Housing Market Outlook Report

This year’s report indicates Canada’s average residential sale price is projected to increase two to three per cent in 2015.

Most regions posted modest gains in average residential sale price, despite increased inventory in many of Canada’s housing markets. Residential property markets in Toronto, Vancouver and their surrounding areas, as well as Calgary and Edmonton continued to see prices and sales rise. The greater areas of Vancouver and Toronto saw inventory of singlefamily houses remain at a record low, while demand continued to climb. Prices in these markets are expected to continue to increase in 2015, by approximately three per cent in the Greater Vancouver Area and four per cent in the Greater Toronto Area. Healthy gains are also anticipated in Kelowna (7%), Victoria (4%), Windsor (5%) and Moncton (6%).

Outside of B.C., Alberta and some areas of Southern Ontario, higher inventory levels was a significant trend characterizing much of the Canadian housing market in 2014. In some markets, the long, cold winter and late start to the spring season created a build-up of listings on the market, which continued to have an impact throughout the year, but also resulted in higher than usual activity in the fall as buyers came back to the market. In many cities in Canada, notably St. John’s, Quebec City, Ottawa and Halifax, increased construction over the past several years contributed to an increase of inventory. However, with construction of new buildings winding down, inventory levels are expected to balance within the next couple of years without having a notable impact on property prices.

With an increased supply of inventory on the market going into the new year, the average sale price is expected to remain stable or rise modestly in most cities in 2015. Montreal (1%), Quebec City (1.5%), Ottawa (1.6%) and Sudbury (1.6%) are expecting a modest rise in average residential sale price, while little change in prices is expected in Winnipeg, Saskatoon and St. John’s.

Condominiums continued to grow their share of the market in many regions. In Toronto and Vancouver, higher prices and limited inventory for single-family homes mean that condominiums are becoming a practical choice for many young buyers looking to enter the market. In Montreal, Kingston, Burlington, and Victoria, condos are increasingly attracting Baby Boomers looking for affordability and amenities within walking distance.

Many first-time buyers continued to feel the impact of the Canada Mortgage and Housing Corporation’s tightened lending criteria, which were revised in 2012. The new mortgage lending regulations have delayed the entry of first-time buyers into the market in many regions, thus slowing down the rest of the market. Regina and Saskatoon were exceptions; well-paying jobs and a good availability of affordable options meant that young buyers were typically able to qualify for a mortgage for their choice of home in these markets. The new mortgage rules will likely have less of an effect in the coming year as buyers adapt to the new regulations and make the necessary changes to meet the criteria.

The historically low interest rates of the past several years have helped sustain demand, and have mitigated the impact of the tightened lending criteria. The Bank of Canada has hinted at a rate increase in late 2015, and some experts have speculated that the increase could come as early as May. An interest rate hike could potentially result in a spike in buying activity, as buyers rush to secure their mortgage before the increase comes into effect. Overall, a rate increase is not anticipated to have a dramatic effect on the real estate market, as it would likely be minor and rates would continue to be low.

The economic outlook for Canada in 2015 is stable. The Bank of Canada has projected GDP to grow by approximately 2.5 per cent, a rate that is roughly on par with 2014’s growth. Small increases in employment rates and wages are anticipated as well. Canada expects to welcome between 260,000 and 285,000 new permanent residents in 2015, which should positively impact the residential real estate market.

Outlook on Calgary:

Calgary’s housing market had another year of healthy price appreciation as the average residential sale price has grown and is expected to finish off 2014 with an approximate six per cent gain to $483,000 from $456,000 in 2013. House price increases have been attributed to good employment in the energy sector driving migration to the city.

A city-wide Civic Census showed that in April 2014, Calgary saw the migration of approximately 28,000 people to the area in the past 12 months, an increase of about 1,800 compared to the previous year. Migration has significantly impacted the real estate market fueling Calgary’s consistent strong performance over the past few years. However, in the fall of 2014, the housing market started to show a shift from a seller’s market to a more balanced market, likely due to a decrease in oil prices.

The price adjustment in the energy industry should likely have an impact on the 2015 Calgary housing market. While it is still expected to see a slight increase in price, it is anticipated to be less active as potential buyers wait to see if lower oil prices result in more favourable house prices. However, RE/MAX expects 2015 to be a balanced market, creating a more level playing field for buyers and sellers. A combination of oil prices and dollar value should have the greatest impact on Calgary’s housing market in 2015.

One advantage is that most oil industry corporations are being paid in the American dollar, thereby lessening the current effect of the low Canadian dollar.

Calgary is projected to see a four percent increase in unit sales and a more modest three per cent increase in average residential sale price increasing to $497,500.

Buyers who are looking to move up are likely to drive demand in Calgary’s real estate market in 2015. Also, the low vacancy rate for rentals has made potential tenants look at purchasing sooner than they anticipated.

Condominiums and townhouses are expected to represent a growing share of the active marketplace, as long as they are priced competitively. With increasing house prices, condominiums and townhouses are an affordable way to purchase real estate in the city.

The city’s growth is prompting optimism for its housing market in 2015. Today, the population is close to 1,195,000, and growing. There is a mild concern as to how the city will keep up with such growth, as new infrastructure will be required. Despite this need, it is anticipated that Calgary’s real estate market should continue to flourish throughout 2015.

For more details and information, check out the Market Outlook for 2015 for all of Canada.

Calgary resale housing market continues to sizzle in October

Second highest MLS sales ever for the month

Average Price of Calgary single-family homes:

Sales in Calgary for single-family homes:

Average price of Calgary condo apartments:

Sales in Calgary for condo apartments:

Calgary’s booming resale housing market showed no signs of slowing down in October as MLS sales reached their second highest level ever for the month while prices continued to gain year-over-year.

According to the Calgary Real Estate Board, total MLS sales in the city during the month increased by 10.22 per cent from last year to 2,147. The median price was up by 5.33 per cent to $430,550 while the average sale price rose by 6.50 per cent to $488,474.

New listings of 2,919 were up 15.79 per cent from October 2013 and active listings at the end of the month increased by 15.28 per cent to 4,428.

“October showed little sign of the housing market slowing down as sales momentum continued this month. Positive sales growth throughout the housing sector was demonstrated largely in part by the record number of luxury home sales as well as a steady resale market,” said Kaitlyn Gottlieb, a realtor with Century 21 Bamber Realty Ltd. “Net migration and population growth, coupled with Calgary’s vast employment opportunity together with comparatively high wages, remain the driving factors behind the price growth Calgarians continue to see.

“Although still below historical norms, improvements in Calgary’s inventory levels and the easing of market tightness has added to listing growth and furthered stability, alongside sales this quarter. As we approach the end of fall, we continue to see a firm confidence in both homebuyers and investors adding to the anticipation that sales will remain at a positive level moving into the winter months.”

Mike Fotiou, associate broker with First Place Realty, said October sales were just behind the all-time record of 2,204 set in 2005 for the month.

Average sale prices in October neared the all-time records of $492,136 for the city which was set in June this year and $567,653 in the single-family market which was established in September.

In October, the single-family home market saw sales of 1,462, up 9.68 per cent year-over-year. The median price rose by 8.41 per cent to $490,000 while the average sale price was up by 7.53 per cent to $555,251.

The condo apartment category had 385 transactions, up 14.24 per cent. The median price rose by 4.04 per cent to $283,000 and the average sale price increased by 4.18 per cent to $322,358.

In the condo townhouse segment, sales of 300 were up by 7.91 per cent from last year. The median price of $333,766 and the average sale price of $376,227 were up 4.71 per cent and 3.70 per cent respectively.

And in the towns outside Calgary market, MLS sales climbed by 27.23 per cent to 486 transactions as the median price was up 7.57 per cent to $387,250 and the average sale price rose by 8.32 per cent to $412,026.

“Even as we enter the traditionally slower season of Calgary real estate, we continue to witness a strong demand,” said Don Campbell, senior analyst with the Real Estate Investment Network. “This demand is being tempered, a bit, by concern surrounding the oil price and thus keeping our market price increase away from the percentages we witnessed in 2006-2007. Away from the statistics, on the street analysis is beginning to show a slowing down in the number of showings, especially in the upper half of the market. This slowdown will reflect into sales statistics over the coming three months and if sales in the higher end of the market are slower, that will keep a cap on the ever-quoted average sale price.”

“Migration to the city continues to be strong bringing low vacancy rates and increasing rents. This means that first-time home buyers continue to prop up the lower end of the market while keeping demand strong.”

CREB also keeps track of what it calls a benchmark price on typical properties sold in the market. The benchmark prices for each housing category as well as percentage annual change are: single-family, $513,500, 9.7 per cent; townhouse, $337,800, 9.7 per cent; apartment, $299,800, 8.6 per cent; composite, $460,700, 9.5 per cent; and surrounding towns, $379,600, 9.43 per cent.

Ann-Marie Lurie, chief economist with CREB, said overall demand continues in the local real estate market.

“We’ve had the strong employment growth. The migration that we’ve seen over the past few years. And now there’s been listings. So there’s been some selection in the market and that’s really encouraged some of that demand,” said Lurie. “We still are in a period of favourable lending rates. All of that is encouraging the sales activity that we’ve seen.

“It hasn’t shown any sign of slowing because we’ve had the listings. What’s really shifted is that the market is more balanced now than it was even three to six months ago.”

CREB’s monthly report said there was only 18 per cent of new single-family listings priced below $400,000 and only 387 remained in inventory by the end of the month.

“All citywide resale segments have recorded a moderate easing of supply constraints, which should help stabilize prices as we approach the end of the calendar year,” said Lurie. “Nonetheless, consumers should be aware that market conditions can vary significantly depending on the location and property type.”

By Mario Toneguzzi, Calgary Herald

Calgary luxury home sales on record pace

Every month this year has set a new peak for MLS transactions

The appetite for luxury homes in Calgary continues to be very strong as another MLS sales record was established in August.

The appetite for luxury homes in Calgary continues to be very strong as another MLS sales record was established in August.

According to the Calgary Real Estate Board, there were 69 properties that sold for $1-million or more during the month, eclipsing the previous monthly high of 64 set last year.

Each month this year has established a record for luxury home sales.

Year-to-date, there have been 611 luxury home sales until the end of August compared with 522 for the same period last year. The all-time peak for annual sales at the $1-million plus level was in 2013 with 726 MLS transactions.

“Bolstered by the city’s thriving economy, the strength of its oil and gas sectors, low unemployment rates, high average net incomes and strong net migration, the market for high-end homes continued its upward trajectory with single-family home sales up 19 per cent and attached home sales up 21 per cent year-over-year,” said Sotheby’s International Realty Canada’s Top-Tier Real Estate Report for the first half of the year, which was released on Thursday.

“Due to limited inventory in Calgary’s condo market, sales decreased 25 per cent compared to the same time last year. With a number of new high-end condo projects recently announced in Calgary’s downtown core, it is expected that the volume of luxury condo sales above $1 million will increase in the second half of 2014.”

Ross McCredie, president and chief executive of Sotheby’s International Realty Canada, said the Calgary housing market is still relatively inexpensive for many people who have moved to the city from other parts of Canada.

“There’s a ton of different factors (to the luxury home boom) but overall there’s a ton of confidence,” he said.

“Low interest rates, a lot of confidence specifically in Calgary where you have a lot of investment, very, very low unemployment and you have huge demand for jobs . . . Overall we don’t see anything that’s going to change in the horizon right now for us.”

The Sotheby’s report said low inventory in the beginning of the year drove bidding wars and price increases in a market that favoured sellers.

“Over the summer months, new inventory over $1 million emerged to meet strong consumer demand, particularly in the condominium market, a trend which is expected to continue into the fall,” it said. “At the same time, Calgary’s robust economy is expected to sustain demand for luxury real estate, and notable growth is expected in the $4 million single-family home market throughout the fall and into 2015 as this category has already outpaced 2013 sales numbers.”

By Mario Toneguzzi, Calgary Herald

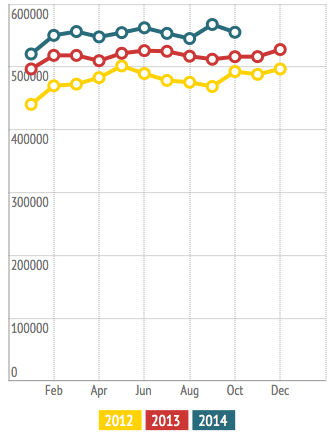

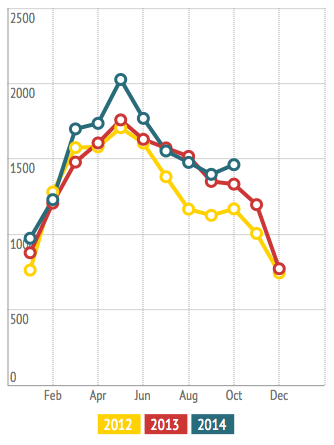

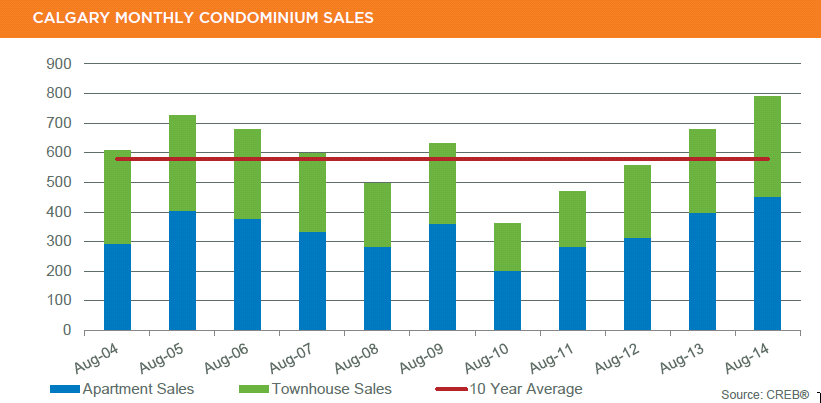

CALGARY REGIONAL HOUSING MARKET STATISTICS – August 2014

Condominium sales set a new record for August activity

Sales activity improves for condominium product, while declining in the single-family sector

Strong gains in Calgary’s condominium apartment and townhouse sectors sparked a 3.4 per cent year-over-year growth in residential resale housing sales activity for August. A total of 2,267 units exchanged hands in the city during the month, compared to 2,192 during the same period in 2013.

The condominium apartment and townhouse sectors saw the biggest gains, increasing by nearly 14 and 20 per cent, respectively, for total monthly sales of 790 units. “The record pace of August sales in the condominium sector is related to the relative affordability of this product combined with a tight rental market and low lending rates,” said CREB® chief economist Ann-Marie Lurie, noting most of the activity continues to take place in lower price ranges.

“More than 76 per cent of condominium new listings are priced below $400,000 and represent more than 68 per cent of the total inventory within city limits.” So far this year, condominium apartment and townhouse sales have totaled a respective 3,388 and 2,685 units. This represents a combined increase of nearly 20 per cent.

“Over the past three months apartment-style new listings have increased by more than 40 per cent year over year, pushing up overall inventory levels and moving this market toward balanced territory despite the strong sales growth,” said Lurie. Meanwhile, year-over-year single-family sales declined by 2.4 per cent in August to 1,477 units, partly due to limited availability in lower price ranges. Despite the pullback, activity in the sector remains stronger than long-term averages.

“The decline in single-family sales is mostly due to the shrinking supply in the under-$400,000 sector,” said CREB® president Bill Kirk. “Overall, sales activity has improved compared to last year for product priced over $400,000.”

The good news for buyers is added choice. New listings in August improved by 13.6 per cent compared to last year, causing inventories to rise by nearly 18 per cent. Increased inventory levels also moved the single-family market toward more balanced conditions, helping minimize further monthly price gains.

The single-family unadjusted benchmark price totaled $512,300 in August, similar to July, but still 10.24 per cent above $464,700 posted a year ago. “Following a prolonged period of Calgary being a sellers’ market, a move toward more balanced conditions is welcome news,” said Kirk.

“This will help support a more stable city housing market in terms of price gains.” The average, median and benchmark prices for condominium apartments in August were a respective $332,006, $287,500, and $298,200. “While both average and median prices in this sector have recorded further monthly gains, the benchmark indicates prices are similar to levels recorded in the previous month,” said Lurie.

“The composition of apartment sales shifted toward the higher-end segment this month compared to last month, resulting in higher monthly gains. The benchmark price reflects price changes for similar properties, less subject to the variability in composition.”

Condominium townhouses remain the tightest of the three sectors in Calgary, resulting in further monthly price gains and reaching an August benchmark price of $328,300. While prices are shy of previous highs, they increased by 0.4 per cent over the previous month and nearly 10 per cent above levels recorded in August 2013.

Click Here to view the full .pdf of the CALGARY REGIONAL HOUSING MARKET STATISTICS – August 2014

Calgary resale housing market experiences highest annual price growth

10.48% hike from a year ago

Calgary continues to far outstrip the rest of the country when it comes to annual price gains in the resale housing market.

The MLS Home Price Index, released Friday by the Canadian Real Estate Association, said prices in the Calgary area in July were up by a whopping 10.48 per cent compared with a year ago. Meanwhile, the national aggregate, comprising 11 centres, saw a year-over-year hike of 5.33 per cent as sales rose to their highest level since March 2010.

The closest centre to Calgary’s annual spike was Toronto which recorded a jump of 7.88 per cent.

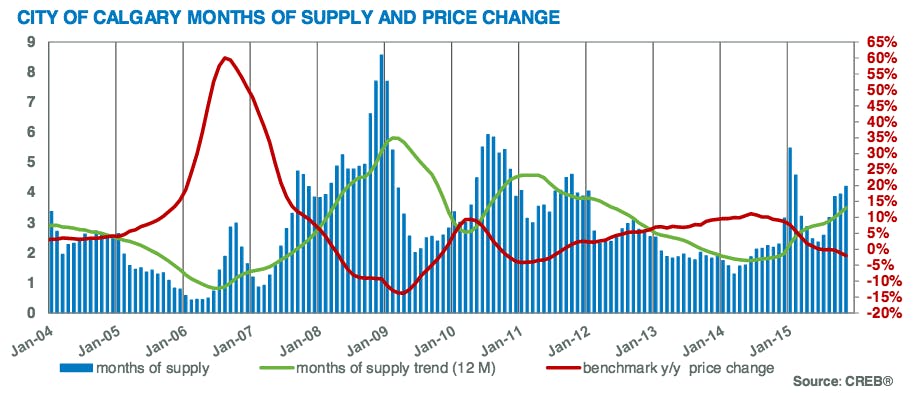

“As market conditions move toward more balanced conditions, it is causing prices to level off. However, due to strong gains in the first half of the year, even with prices levelling off, year-over-year gains remain at higher levels,” said Ann-Marie Lurie, the Calgary Real Estate Board’s chief economist.

Over the past three years, Calgary also has the highest rate of price growth at 25.01 per cent compared with 12.52 per cent nationally. And over five years, Calgary’s 28.89 per cent spike is second only to Toronto’s 40.48 per cent increase while it is 26.89 per cent across the country.

Don Campbell, senior analyst with the Real Estate Investment Network, said it takes 18 months for immigration and population growth to begin to affect the resale and new housing markets. Also, a demand/supply imbalance has contributed to higher prices.

He said the housing market is being affected by tightness in rental vacancy and lack of new supply.

“So the record population growth we witnessed last year is now being felt,” he said.

“Combine this with a general decrease in available single-family home building lots and this is keeping the inventory tighter than normal, thus adding upward value pressure on resale market.”

The number of homes sold nationally through the MLS systems of Canadian real estate boards and associations rose to 48,000 in July – a 7.2 per cent hike from a year ago.

Calgary area sales of 3,177 were 6.8 per cent higher and Alberta sales of 7,194 were up 5.0 per cent.

“Low mortgage interest rates continue to bolster home sales activity,” said Gregory Klump, CREA’s chief economist, in a news release. “With the Bank of Canada widely expected to hold interest rates steady until next year, home purchase financing will remain attractive over the second half 2014 and continue to support economic growth while waiting for Canadian exports and investment to improve.”

In terms of average MLS sale prices, Calgary saw a rise of 5.2 per cent year-over-year to $460,790 while the increase was 4.2 per cent in Alberta to $395,552 and 5.0 per cent across the country to $401,585.

Leslie Preston, economist with TD Economics, said low interest rates are continuing to fuel the Canadian housing market into the summer.

“The renewed momentum in Canada’s housing market in recent months represents both a bounce back from weather-related weakness over the winter months and a response to lower mortgage rates,” explained Preston. “Potential buyers who may have sat on the sidelines last year as interest rates rose, are being enticed back to the market by lower interest rates. Meanwhile, a strengthening in economic growth continues to support the fundamental demand in the housing market.

“However, existing home prices . . . are on track to outstrip income growth for a second straight year in 2014, which adds to concerns about an already-overpriced market. Affordability, even at low interest rates, has become an obstacle in many markets. This contributes to our view that the Canadian housing market will cool later this year and into 2015 as interest rates are likely to nudge higher. Another factor which is expected to weigh on prices is the supply growth in the pipeline due to the record number of new homes that are under construction in many markets.”

By Mario Toneguzzi, Calgary Herald

Calgary region housing starts to increase 24% in 2014

But decline almost 8% in 2015

Increased demand and a low level of supply are pushing housing starts in the Calgary region to an elevated level this year.

Housing starts in the region are forecast to rise by 24 per cent in 2014 from last year but then dip by 7.7 per cent in 2015, according to a new report released Wednesday by Canada Mortgage and Housing Corp.

The agency’s housing outlook says starts in the Calgary census metropolitan area will increase from 12,584 in 2013 to 15,600 this year but then fall to 14,400 next year.

“The rise in total housing starts this year is due to a combination of increased demand and a decline in supply,” said Richard Cho, senior market analyst in Calgary for the CMHC. “Employment growth in Calgary continues to post impressive gains with the majority in full-time positions. Low mortgage rates have also helped people purchase a home and migration has been elevated in the last couple of years. This has supported the demand for housing. Selection in the resale market has been low which has led to some prospective buyers to look to the new home market. Not only are active listings low but new home inventories are down, which will also contribute to the rise in construction this year.

“In 2015 total housing starts are forecast to decline but still reach its second highest level since 2006. Job creation in Calgary is forecast to moderate from the elevated pace in 2014 and net migration, although remaining positive, will decline as economic conditions improve in other areas of the country. We are also anticipating that buyers will have more homes to choose from as average monthly active listings are expected to be higher. The number of new homes under construction has increased and may put more upward pressure on inventories when completed. This will impact the opportunity to increase new construction in 2015.”

For Alberta, starts are forecast to increase by 7.2 per cent this year to 38,600 units but decline by 4.7 per cent next year to 36,800 units.

The agency is expecting MLS sales in the Calgary region to improve by 9.8 per cent this year to 32,900 units and by another 2.4 per cent in 2015 to 33,700 transactions. CMHC says the average MLS sale price will rise by 5.0 per cent in 2014 to $459,000 and by 2.8 per cent in 2015 to $472,000.

“The economy in Calgary is anticipated to continue creating jobs, attracting migrants and supporting income growth,” said Cho. “However, the rate of increase in some of these key housing demand factors will moderate throughout the forecast period. This will also be reflected in the resale market.

“Home prices in Calgary have experienced more upward pressure from the low supply of active listings on the market compared to previous years. Buyers have been competing for a lower selection of homes, resulting in multiple offers on many homes and shortening the average days-on-market. The MLS price is forecast to rise five per cent in 2014. As we move towards the end of 2014 and into 2015, the supply of resale homes is anticipated to move higher. New listings in Calgary have started to pick up and are forecast to rise this year and next. This will help ease some of the upward pressure on prices in 2015 resulting in a 2.8 per cent increase.”

For Alberta, MLS sales are forecast to be 5.8 per cent higher this year to 69,900 followed by a 2.9 per cent gain next year to 71,900.

The average sale price in the province is expected to increase by 4.2 per cent this year to $396,800 and by 2.6 per cent next year to $407,000.

Housing starts in the region are forecast to rise by 24 per cent in 2014 from last year but then dip by 7.7 per cent in 2015, according to a new report released Wednesday by Canada Mortgage and Housing Corp.

The agency’s housing outlook says starts in the Calgary census metropolitan area will increase from 12,584 in 2013 to 15,600 this year but then fall to 14,400 next year.

“The rise in total housing starts this year is due to a combination of increased demand and a decline in supply,” said Richard Cho, senior market analyst in Calgary for the CMHC. “Employment growth in Calgary continues to post impressive gains with the majority in full-time positions. Low mortgage rates have also helped people purchase a home and migration has been elevated in the last couple of years. This has supported the demand for housing. Selection in the resale market has been low which has led to some prospective buyers to look to the new home market. Not only are active listings low but new home inventories are down, which will also contribute to the rise in construction this year.

“In 2015 total housing starts are forecast to decline but still reach its second highest level since 2006. Job creation in Calgary is forecast to moderate from the elevated pace in 2014 and net migration, although remaining positive, will decline as economic conditions improve in other areas of the country. We are also anticipating that buyers will have more homes to choose from as average monthly active listings are expected to be higher. The number of new homes under construction has increased and may put more upward pressure on inventories when completed. This will impact the opportunity to increase new construction in 2015.”

For Alberta, starts are forecast to increase by 7.2 per cent this year to 38,600 units but decline by 4.7 per cent next year to 36,800 units.

The agency is expecting MLS sales in the Calgary region to improve by 9.8 per cent this year to 32,900 units and by another 2.4 per cent in 2015 to 33,700 transactions. CMHC says the average MLS sale price will rise by 5.0 per cent in 2014 to $459,000 and by 2.8 per cent in 2015 to $472,000.

“The economy in Calgary is anticipated to continue creating jobs, attracting migrants and supporting income growth,” said Cho. “However, the rate of increase in some of these key housing demand factors will moderate throughout the forecast period. This will also be reflected in the resale market.

“Home prices in Calgary have experienced more upward pressure from the low supply of active listings on the market compared to previous years. Buyers have been competing for a lower selection of homes, resulting in multiple offers on many homes and shortening the average days-on-market. The MLS price is forecast to rise five per cent in 2014. As we move towards the end of 2014 and into 2015, the supply of resale homes is anticipated to move higher. New listings in Calgary have started to pick up and are forecast to rise this year and next. This will help ease some of the upward pressure on prices in 2015 resulting in a 2.8 per cent increase.”

For Alberta, MLS sales are forecast to be 5.8 per cent higher this year to 69,900 followed by a 2.9 per cent gain next year to 71,900.

The average sale price in the province is expected to increase by 4.2 per cent this year to $396,800 and by 2.6 per cent next year to $407,000.