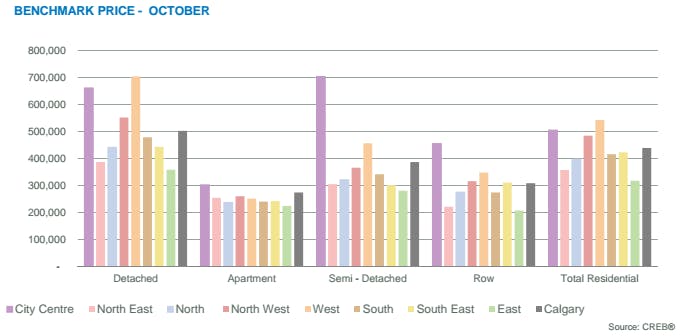

Detached prices stabilize in soft market

For the first time in two years, sales activity in October resembled normal levels. City-wide sales totaled 1,644 units, which is an increase of nearly 16 per cent over last year.

“The shift in sales activity this month is likely related to the new mortgage rule changes, inventory gains in the lower price ranges and further price adjustments,” said CREB® chief economist Ann-Marie Lurie. “The combination of all these factors may have encouraged some purchases to take advantage of the market conditions, particularly in the lower price ranges. However, with several factors at play, the monthly shift in demand may be temporary and will need to be monitored over the next several months.”

Sales activity rose across all product types in comparison to last year, but the largest gain in sales occurred in the detached sector at 18 per cent.

There was a noticeable shift in sales activity by price range in October. In the detached market, homes priced between $300,000 and $400,000 saw the largest improvement in sales, while attached and apartment sales growth was mainly occurring in the lower price ranges.

“This year has been a challenge for many sellers,” said CREB® president Cliff Stevenson. “So when we have a rise in sales, it means more buyers got into the market and more sellers got out, which is a positive for consumers on both sides of the transaction.”

“Sales activity changed direction in October, but we need to see some consistency next month and the month after to call it a trend,” adds Stevenson. “For now it’s a nice building block.”

Despite the monthly rise, year-to-date sales activity in all sectors remained lower than last year’s levels and well below longer term trends. In fact, year-to-date sales activity has totaled 15,642 units, which is 6.3 per cent below last year’s levels. While increased activity in the lower price ranges had a greater impact on the average and median price, benchmark prices once again edged down in October.

The city-wide unadjusted benchmark price totaled $438,900, or 0.34 per cent below last month and four per cent below last year’s levels.

Since the start of the downturn, home prices have declined from a low of 3.8 per cent in the detached market to a high of 9.4 per cent in the apartment condominium sector. And, despite the rise in October sales, monthly prices continued to decline for most product types in the market.

Click on the following link to view the full .pdf report! October-2016-statistics-package-for-the-city-of-calgary

Click on this following link to view the full .pdf report for the Regional Statistics: october-2016-regional-statistics-package-for-calgary-and-area

housing report

Alberta housing market a standout performer

Underlying driver is a robust economy

Alberta has emerged as a standout performer in Canada’s housing market and while a slowdown in Canada’s broader housing market is underway, the province’s housing sector has been heating up, says a new report.

The Alberta Treasury Board and Finance’s Economic Spotlight said housing starts continue to trend higher, prices are accelerating, and the resale market remains firmly in seller’s territory in the province.

“The underlying driver is a robust economy. Alberta’s economy has grown at double the rate of the Canadian average over the past three years, and accounted for a disproportionately high share of the nation’s new jobs,” said the report. “Job opportunities have lured migrants from other provinces, creating a need for new housing, while rising wages have kept affordability in check.

“Record inflows of migrants have also resulted in a tighter rental and resale housing market, pushing activity and prices higher. On the supply side, the flooding in Southern Alberta has reduced the stock of available homes, adding further tightness to the market.”

The report said Alberta’s low unemployment rate and higher average wages will continue to draw inmigrants, both from within and outside Canada.

“These new migrants tend to be younger, workingaged adults,” it said. “The transitioning of these new young migrants from rental accommodations into home ownership will be a primary driver in the housing market demand. Higher wages will also encourage continued household formation and home ownership.

“Net migration is forecast to remain high over the near term and will be an important driver of housing demand. After spiking by 3.5 per cent in 2013, the largest increase since 1981, Alberta’s population growth is forecast to ease to a stillstrong 2.9 per cent in 2014 before gradually moving to 2.0 per cent by 2017.”

The report said housing is expected to remain a vibrant part of the Alberta economy, but there are risks to the outlook.

With a commodity-driven economy, a slowdown in emerging markets could lower prices and impact Alberta, leading to lower in-migration and lower housing demand.

The report also said housing affordability is also a risk and an unexpected shift in the trend of higher wages and lower interest rates would impact the market.

“On the upside, the housing market could also strengthen more than expected. A stronger-than-forecast expansion in Alberta could lead to more in-migration, and put further pressure on housing demand,” said the government report.

“The housing market in Alberta performed exceptionally well through 2013 and is forecast to strengthen further in 2014, at a time when the national housing market is expected to slow or level off.”

In another report, Diana Petramala, economist with TD Economics, said “Calgary is one market that appears to be more balanced than the rest and has more upward potential.”

By Mario Toneguzzi, Calgary Herald

Market Trends: Farm Edition 2013

Click here on the image above to view the full report: Canada wide!

Click here on the image above to view the full report: Canada wide!

Central Alberta

Low interest rates and record crops continue to fuel demand for farmland from Kneehill north to Red Deer Counties, with the number of parcels transferring ownership in the 12-month period ( June 2012 to May 2013) on par with last year’s strong performance. Inventory continues to be a challenge in the area, with the shortage placing serious upward pressure on values. Price per acre has increased about 15 per cent on average this year over last, with prime land fetching substantially more. Properties that would have sold at an average of $2,800 to $3,500 an acre one year ago now have a sticker price as high as $3,400 to $4,500 per acre, or as high as $5,500 an acre in Olds. In the Lacombe area near Red Deer, even greater pressure exists, with values rising to as high as $6,500 per acre. Private deals continue unabated between neighbours and landlords/tenants, further hampering listing inventory. By far, the most aggressive players in the market are the supply-managed farms and the Hutterite Colonies—both of whom are looking to expand existing operations. New players have also emerged in recent years, including the investment community, who are now diversifying portfolios to include agricultural land

Many are opting for 3,000 acres to start, with land ideal for cereal grains, including wheat, canola, and barley. Interest rates continue to play a crucial role in the compilation of farmland, with variable rates hovering at two to three percent. Some farmers, anticipating higher rates down the road, are locking in at five- and ten-year terms to secure more long-term favourable rates. The low interest rate environment has discouraged some people from selling their land (unless they can sell at a premium), ultimately limiting the amount of land for sale. Yet, it has also created confidence amongst buyers that can now budget their cash flow to service new debt. Managing risk continues to be a mainstay for those in farming, with many lending institutions now working alongside agricultural communities. One trend that has been supported by loans offered by Farm Credit Canada (FCC) and other financial institutions is the return of younger farmers back into the market. Tremendous crops and record commodity prices in recent years have been a major impetus, in spite of commodities off last year’s peak levels. While market conditions are expected to remain stable for the remainder of the year in Central Alberta, the rapid appreciation experienced in the past is unlikely to continue. Banks are expected to somewhat tighten lending practices in the coming year, which will further serve to slow escalation. Still balance sheets show strong equity across the board, one factor that will support the market for farmland in the months and years ahead.

Southern Alberta

A serious shortage of farmland listings continues to temper momentum in Southern Alberta’s market. Buyers continue to seek out cultivated, dry land and irrigated parcels, but available properties remain few and far between. Approximately 10 farmland listings are currently available for sale. Exclusive listings and private deals continue to be commonplace, keeping listings from the open market and an expanded buyer pool. Any quality sections that have come on stream have moved quickly, and although demand remains strong, lower commodity values have served to create a new level of diligence among buyers. Purchasers are weighing their options and waiting for the ideal parcel. However, when the right opportunity presents, they’re moving quickly. Most farmland properties generally sell within two weeks—some within days. Confidence remains high and most purchasers feel secure in long-term value and potential that farmland investment represents. The bulk of buyers are local end users. The need and desire to expand continues to bolster the market, as everyone from smaller operators, local Hutterite colonies and major players vie to increase their stake. Some U.S. investors have bought up parcels for a long-term hold, with the intent to rent the land to existing operators. Competition for rental land remains solid, with rents averaging $50 to $60 an acre for dry land, while irrigated land with pivot commands a premium. While supply outpaces demand, prices have managed to hold firm over the past year. Grassland is commanding $800 to $1,200, while dry, bare land typically generates $1,000 to $1,600 per acre. Irrigation land requires a premium outlay, usually moving between $5,000 and $8,500 per acre. Farmland closer to key cities/municipalities have garnered top dollar, with notable sales this season running between $9,200 and just under $10,000 an acre. Deals are coming together rather fluidly, as most vendors continue to have realistic expectations. Financing is rarely an issue, despite tighter lending restrictions. Buyers exist for virtually all types of product, from large parcels to quarter sections, gentleman/hobby farms to ranchland and dairy operations, as long as the price reflects fair market value.

To date, the board has recorded roughly three dozen sales, with the busiest season for farmland real estate set to get underway this fall. While the pace remains steady, there are few multiple offers to speak of, as most properties sell right away through word of mouth, either exclusively or in private deals. Or in the case of MLS listings, most realtors have their own willing buyer pool waiting in the wings. Despite news of widespread flooding in Southern Alberta earlier this spring, most crop land was unaffected, although some hail did damage crops in the southeast area of the province. On the whole, yields look good for 2013. Overall, vendors can expect demand to remain in line with current levels for the foreseeable future, while purchasers will benefit from price stability. The potential for rising interest rates is not expected to prove a significant deterrent to eager purchasers, whose belief in land remains steadfast.

Click Here to view the full report for all of Canada.

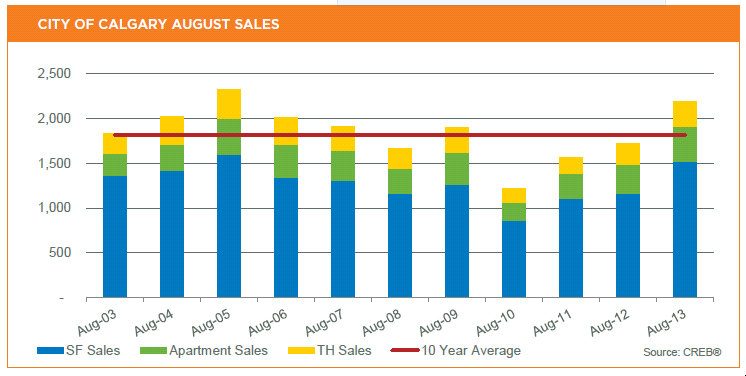

CALGARY REGIONAL HOUSING MARKET STATISTICS for August 2013

SUMMER SALES STAY STRONG

Seller’s market conditions persist, pushing up prices

(click on the photo above to download the full report)

Residential sales within city limits totaled 2,196 units, an 27.5 per cent increase over 2012 and 8.7 per cent on a year-to-date basis.

The level of transactions was well above long-term trends for the month, mostly due to improved activity in the single-family sector. However, on a year-to-date basis, activity is only slightly higher than expectations.

“The sales have been limited by the need for more resale listings,” said CREB® President Becky Walters. “However, August did see more new listings than last year, giving buyers more choice.”

August new listings recorded a year-over-year improvement of 7.4 per cent. While seller’s market conditions persist and total inventory levels keep falling, improvement in new listings helped prevent further tightening in the market despite the sales growth.

Single-family sales totaled 1,517 units in August, a 30 per cent increase over the previous year. Despite strong sales in the past couple of months, year-to-date sales activity has grown by 5.4 per cent, slightly stronger than anticipated.

Click on the following link to download the full report of the Monthly Housing Statistics for August.

City's housing affordability 'among better in Canada'

Calgary’s housing market appears to have weathered the worst floods in memory with the second-strongest quarterly sales gain in four years, says the Royal Bank.

“A strong provincial economy, solid labour market, fast-rising population, and attractive affordability continue to fuel demand for Calgary housing,” said the bank’s latest Housing Trends and Affordability Report, to be released Tuesday.

The RBC report, which measured the April to June period, said monthly resale activity increased for six straight months, including in June (rising 1.1 per cent month-overmonth) and July (up 3.1 per cent). On a quarterly basis, home resales rose 12 per cent.

“While prices recently embarked on a more steeply upward trajectory, the effect of faster-rising prices has yet to undermine affordability in any material way,” said RBC. “In fact, affordability levels in Calgary continue to be among the better in Canada.”

The RBC affordability index determines the proportion of median pretax household income needed to service the cost of mortgage payments, property taxes and utilities.

Its measures for Calgary showed little movement in the second quarter, with two-storey homes rising by 0.5 percentage points to 33.6 per cent, while condominium apartments edged lower by 0.2 percentage points to 19.4 per cent.

And while the report cautions home ownership has become less affordable for the average Canadian, RBC said Alberta homebuyers continued to enjoy a relatively affordable housing market.

“Despite the fact that the market has kicked into higher gear since spring – thereby boosting prices and increasing ownership costs – Alberta continues to be a relatively affordable market,” said Craig Wright, senior vice-president and chief economist with RBC. “We will likely see some disruptions in market activity trickle through in summer data from the floods in southern Alberta; however, we anticipate the strong provincial economy will endure, supporting further housing growth in 2014.”

Nationally, during the second quarter, affordability measures rose for two of the three categories of homes tracked. RBC’s measure for the detached bungalow rose 0.3 percentage points and for the standard two-storey home rose 0.4 percentage points to 42.7 per cent and 48.4 per cent, respectively. The measure for the standard condominium was unchanged at 27.9 per cent.

Vancouver’s affordability measure gained 2.2 points to 82.1 on a detached bungalow, while Toronto’s increased half a point to 54.5.