This year’s report indicates Canada’s average residential sale price is projected to increase two to three per cent in 2015.

Most regions posted modest gains in average residential sale price, despite increased inventory in many of Canada’s housing markets. Residential property markets in Toronto, Vancouver and their surrounding areas, as well as Calgary and Edmonton continued to see prices and sales rise. The greater areas of Vancouver and Toronto saw inventory of singlefamily houses remain at a record low, while demand continued to climb. Prices in these markets are expected to continue to increase in 2015, by approximately three per cent in the Greater Vancouver Area and four per cent in the Greater Toronto Area. Healthy gains are also anticipated in Kelowna (7%), Victoria (4%), Windsor (5%) and Moncton (6%).

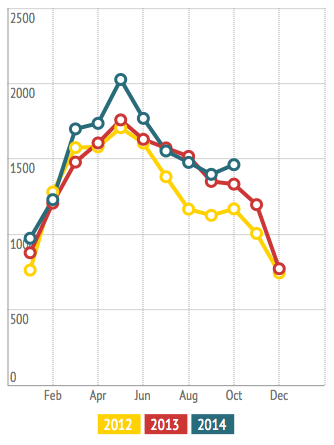

Outside of B.C., Alberta and some areas of Southern Ontario, higher inventory levels was a significant trend characterizing much of the Canadian housing market in 2014. In some markets, the long, cold winter and late start to the spring season created a build-up of listings on the market, which continued to have an impact throughout the year, but also resulted in higher than usual activity in the fall as buyers came back to the market. In many cities in Canada, notably St. John’s, Quebec City, Ottawa and Halifax, increased construction over the past several years contributed to an increase of inventory. However, with construction of new buildings winding down, inventory levels are expected to balance within the next couple of years without having a notable impact on property prices.

With an increased supply of inventory on the market going into the new year, the average sale price is expected to remain stable or rise modestly in most cities in 2015. Montreal (1%), Quebec City (1.5%), Ottawa (1.6%) and Sudbury (1.6%) are expecting a modest rise in average residential sale price, while little change in prices is expected in Winnipeg, Saskatoon and St. John’s.

Condominiums continued to grow their share of the market in many regions. In Toronto and Vancouver, higher prices and limited inventory for single-family homes mean that condominiums are becoming a practical choice for many young buyers looking to enter the market. In Montreal, Kingston, Burlington, and Victoria, condos are increasingly attracting Baby Boomers looking for affordability and amenities within walking distance.

Many first-time buyers continued to feel the impact of the Canada Mortgage and Housing Corporation’s tightened lending criteria, which were revised in 2012. The new mortgage lending regulations have delayed the entry of first-time buyers into the market in many regions, thus slowing down the rest of the market. Regina and Saskatoon were exceptions; well-paying jobs and a good availability of affordable options meant that young buyers were typically able to qualify for a mortgage for their choice of home in these markets. The new mortgage rules will likely have less of an effect in the coming year as buyers adapt to the new regulations and make the necessary changes to meet the criteria.

The historically low interest rates of the past several years have helped sustain demand, and have mitigated the impact of the tightened lending criteria. The Bank of Canada has hinted at a rate increase in late 2015, and some experts have speculated that the increase could come as early as May. An interest rate hike could potentially result in a spike in buying activity, as buyers rush to secure their mortgage before the increase comes into effect. Overall, a rate increase is not anticipated to have a dramatic effect on the real estate market, as it would likely be minor and rates would continue to be low.

For more details and information, check out the Market Outlook for 2015 for all of Canada.

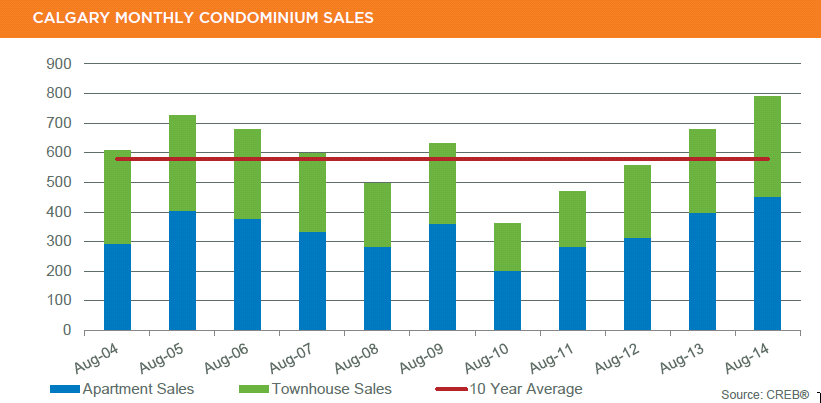

The appetite for luxury homes in Calgary continues to be very strong as another MLS sales record was established in August.

The appetite for luxury homes in Calgary continues to be very strong as another MLS sales record was established in August.